What Is Mat Tax Guru

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Minimum Alternate Tax Mat Section 115jb

Advance Tax Under Income Tax A Complete Guide

Strategic Analysis Of Amended Corporate Tax Rate Regime

Section 115baa And 115bab New Tax Rate For Companies

Itr 7 Indian Income Tax Return Taxguru

The minimum alternative tax mat is a provision introduced in direct tax laws to limit the tax deductions exemptions otherwise available to taxpayers so that they pay a minimum amount of tax to the government.

What is mat tax guru.

Taxability Of Education Cess Issues Relating To Its Computation

Section 115jb Of Income Tax Act 1961 After Budget 2016

32 Income Tax Amendments Assessment Year 2020 21

Income Tax Rates For Financial Year 2019 20 And 2020 21

Tax Guru Taxation Laws Simplified Income Tax Act 1961 Ay 2020 21for B Com Bba

All About Deferred Tax And Its Entry In Books

Interest Payable U S 234a 234b 234c

Functionally Comparable Company Cannot Be Excluded From Comparables For Non Disclosure Of Rpt

Income Tax Incentives And Startup India Benefits Summary

Income Tax Amendments New Provisions Of Finance Act 2020

New Income Tax Regime Beneficial For You

Key Highlights Of Union Budget 2020 21 Finance Bill 2020

Penalties Under Income Tax Act 1961

Income Tax Rates For Financial Year 2020 21 Ay 2021 22

Direct Tax Compliance Calendar

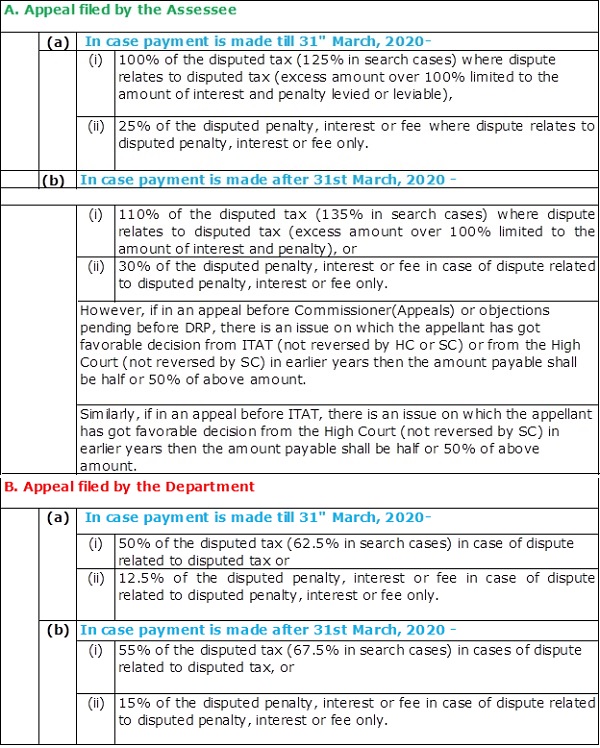

Direct Tax Vivad Se Vishwas Scheme 2020 Detailed Analysis

Set Off Of Bf Loss Mat Credit Adjustments Under New Tax Regime

Employee Share Based Payments And Its Taxation Aspects

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcrkvmluggbegfzohh3cvxqsbxqgtztelw T6refsnbvg6iqahc8 Usqp Cau

Income Tax Rate For Companies For Assessment Year 2020 21

Determination And Accounting Of Deferred Tax Asset And Liability

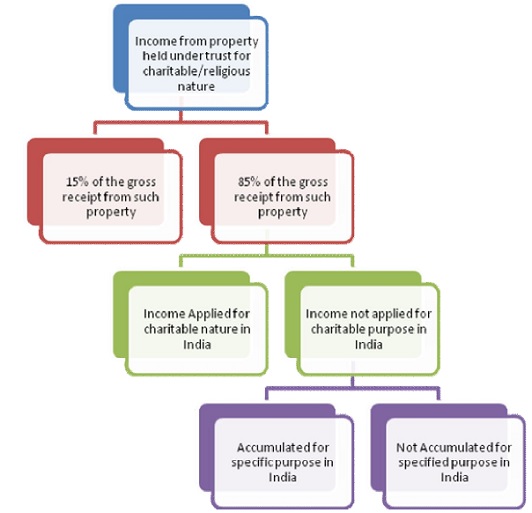

Taxation Of Charitable Religious Trust

Deduction Under Section 80ia 80ib Case Laws Assessment

Section 80 Iba Affordable Housing Scheme Income Tax Deduction

Source : pinterest.com